Paying for Predictability: Why the Business Case for Supply Chain Investment Keeps Failing

Supply chain leaders broadly accept that the operating environment has changed. The question of how to restore stability has given way, for most of them, to a harder one: how to design for an environment in which stability is no longer the baseline. That shift in framing — which James Moffatt explored in an earlier BestPractice.Club piece, From Stability to Predictability — has real implications for how investment decisions get made, and for why so many of them don't.

The problem is not that supply chain leaders lack a diagnosis. Most of them can describe the situation and its consequences. The problem is that the business case for doing something about it keeps failing — not because the argument is wrong, but because of how investment decisions actually get made inside large organisations.

A BPC online roundtable on 23 April, hosted by James Moffatt of Baringa, surfaced that problem in some detail. This is a synthesis of what the group found.

From cost-out to value creation — and why it hasn't solved anything

For most of the past decade, the standard advice to supply chain leaders trying to secure investment was to shift the framing: away from cost reduction and towards value creation. The cost-out business case, the argument went, was too easy to challenge and too hard to prove in practice. A resilience or capability argument, packaged as growth enablement or risk mitigation, would land better with boards.

There is something in this, and several practitioners in the room had made exactly that shift. But it has not resolved the underlying problem. If anything, it has introduced new ones.

The difficulty with a value-creation framing is that it tends to position supply chain investment as a supporter of growth rather than a direct driver of it. Finance teams understand that distinction, and they apply it. When capital allocation decisions are made, growth-enabling projects draw the first tranche. Supply chain, even when articulated as an enabler of growth, tends to be treated as a cost of the business rather than a bet on it. One practitioner described the outcome directly: the investment case is dismissed not because it is unprofitable but because it is not profitable in the right way. You are still being asked to make things cheaper and better; the funding just does not follow.

The underlying issue, as James observed, is structural. Competition for capital has intensified considerably. Cybersecurity now absorbs a significant share of investment that five years ago would barely have featured on a board agenda. Digital transformation programmes, workforce restructuring, and growth initiatives all draw from the same pool. Supply chain cost and resilience programmes — even well-argued ones — are competing in an environment where the case for them is harder to make compelling than the alternatives, most of which have shorter payback horizons and more visible outputs.

It is worth noting that this does not appear to be a problem of supply chain leaders failing to make the case. PwC's 2025 Digital Trends in Operations Survey found that 92% of operations and supply chain leaders cite at least one reason why technology investments have not fully delivered expected results, with integration complexity and data issues as the most common explanations. Notably, an unclear business case was one of the least selected reasons, which PwC flags as a potential blind spot: the people closest to the investment may not be the ones who most clearly see the gap between what is being asked for and what would actually justify it.

The soft benefits problem

The business case problem is not just about framing. It is also about proof.

Several practitioners in the room described a version of the same situation: making a case, getting partial approval or conditional support, implementing something, and then being unable to demonstrate where the benefit landed. The pressure to prove it follows quickly, and the inability to do so erodes the credibility needed to go back for more.

This is not a failure of implementation. It reflects something structural about how supply chain value works. Benefits are typically diffuse, interdependent, and sensitive to context. A range reduction programme might free up inventory — but if the business simultaneously pushes for new product launches, expands into new markets, and changes its service commitments, the inventory signal is buried. The performance of the P&L in the year following a supply chain initiative tells you very little about whether the initiative worked, because nothing else stood still.

Finance teams know this, which is why they ask the question anyway. And supply chain teams know it too, which is why the ask tends to arrive pre-weakened — hedged, caveated, and positioned as "efficiency" rather than made as the harder claim that it actually is.

One practitioner identified a related trap: the habit of presenting business cases in supply chain language to people who think they already understand supply chain. Boards and leadership teams at director and above are not, in most cases, unfamiliar with the concept of a supply chain. But familiarity is not the same as understanding the trade-offs, and the assumption that they get it — on both sides of the conversation — means the hard work of explanation often does not happen. The supply chain team does not translate. The board does not engage. The case fails not because of the argument but because of the gap between how the problem is understood on one side of the room and the other.

Loss aversion as a lever

One shift in approach that James has observed working is a move away from presenting investment options as value-or-nothing choices towards framing them as value-or-risk.

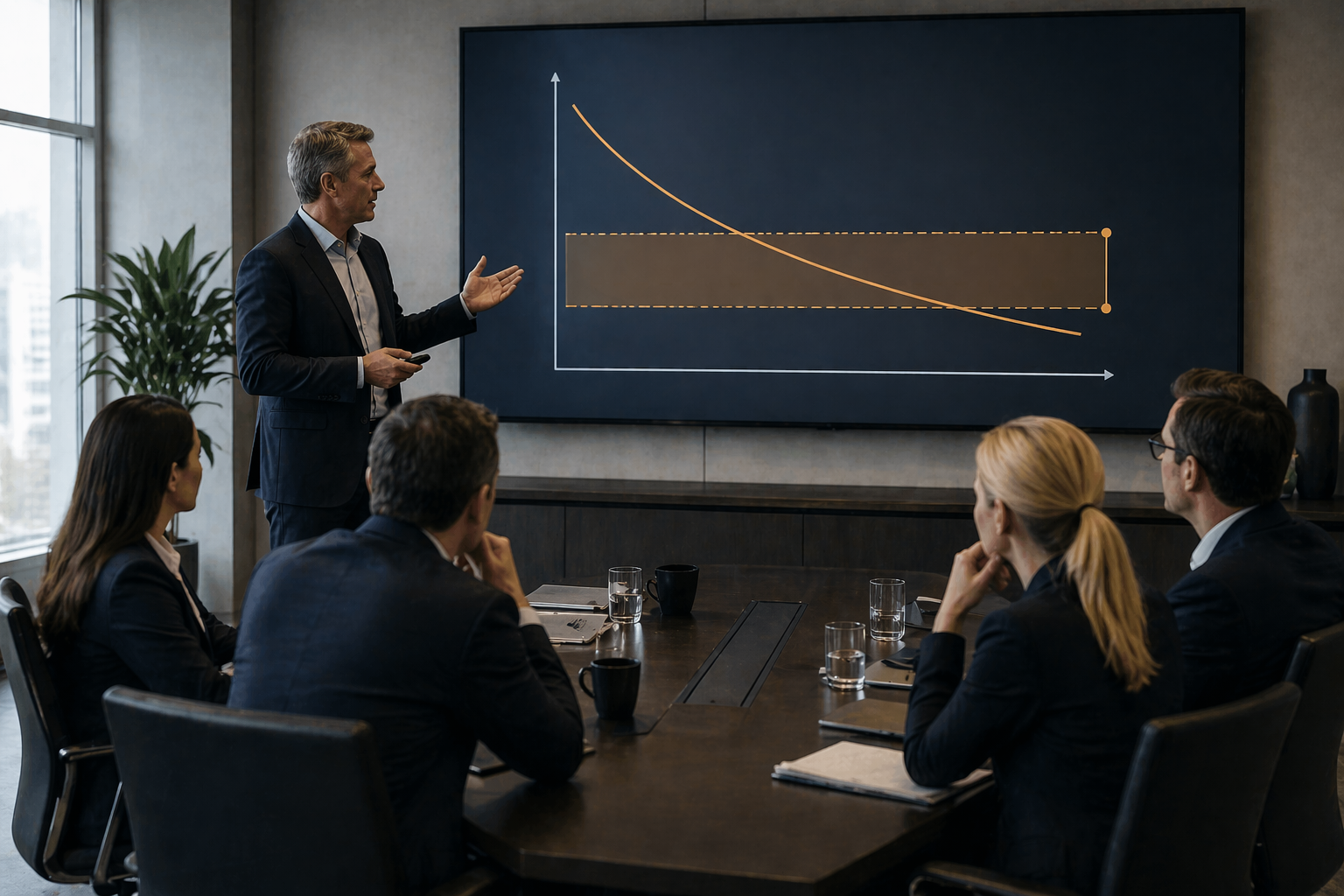

The distinction matters for how decisions get made. When a board is presented with a supply chain investment programme, the alternative they are implicitly choosing between is: invest, or don't invest and assume things will be roughly fine. Most boards, in most conditions, will find a way to justify the latter. Capital is scarce, priorities compete, and the supply chain programme will still be there next year.

The framing shifts when the "do nothing" option is made explicit and costed. Not as a rhetorical move, but as a genuine analysis: this is what the margin trajectory looks like if current cost trends continue and no structural changes are made; this is the operating risk exposure if key dependencies are not addressed; this is the rate at which the business is degrading its long-term position while optimising its short-term one. Presented that way, the choice is no longer between investment and comfortable inaction — it is between investment and a named, quantified downside.

As James put it during the session: "no choice is not an option." The supply chain team's job is to make that clear before the vote, not discover it afterwards.

The cyber attacks of 2025 illustrated the same mechanism in a different context. The M&S attack caused an estimated £300m profit impact from lost sales and operational disruption — not a direct attack on M&S systems, but one that reached them through a third-party supplier. JLR's attack in August halted UK production for five weeks, with revenues falling by more than £1 billion for the quarter. Both businesses had supply chain dependencies that had never been seriously stress-tested, and the cost of that gap became visible all at once. The pattern across 2025 prompted observers to describe it as a tipping point for how boards in the UK think about supply chain risk — not because the risk was new, but because the consequences finally arrived in a form that could not be deferred or explained away.

Supply chain resilience carries the same dynamic, less visibly. The cost of under-investment accumulates in ways that are easy to attribute elsewhere — to market conditions, to demand volatility, to competitor pressure — until the point at which it isn't. The question is whether supply chain leaders can make that trajectory credible to boards before the event that makes it obvious, rather than after.

Packaging and the escape hatch

Even with the right framing, there remains the practical problem of how to present a business case that reflects the interconnected nature of supply chain investment.

The instinct of most organisations is to evaluate projects individually. An automation programme, a planning technology deployment, a supplier diversification initiative — each gets its own ROI calculation, its own approval pathway, its own review cycle. The result is that projects which depend on each other to work are assessed as if they don't. Those that look weaker in isolation (often the foundational ones: the capability investments, the data infrastructure) get cut first. The remaining projects then deliver less than they would have, because the dependencies that made them viable have been removed.

James described an approach used with two different clients in which the supply chain investment case was packaged as a multi-year programme and presented to the board as a coherent whole. The specific tactics differed, but the logic was consistent: make it clear that the programme cannot be arbitrarily disaggregated without losing the value that makes the investment worthwhile, and then give the board a way to commit without committing irrevocably.

In one case that meant a ten-year transformation programme structured with annual tranches and a genuine exit option each year. The board preferred that (a long-term commitment with periodic off-ramps) to the usual pattern of one-off approvals that might or might not arrive. In another, it meant presenting the full supply chain picture of the organisation, showing the scope and interdependency, and framing the choice as between the whole programme and the cost of the status quo — not between individual projects and their immediate alternatives.

This approach has a failure mode, which at least one practitioner in the room had experienced: bundle the case, set the "all or nothing" condition, and lose. If the board does not accept the framing — if the programme is characterised as non-core, or assessed against a growth lens it cannot satisfy — the whole package goes, and the credibility to try again is diminished. It is not a risk-free strategy.

But the underlying logic remains sound. Supply chain investment cases evaluated in isolation tend to understate the value and overstate the difficulty. The work required before a case like this can be made is substantial: a clear picture of the current margin trajectory, a shared view of what the target operating model is trying to achieve, an honest assessment of data and capability maturity, and — critically — a leadership team that has been prepared for the conversation before it happens rather than encountering the argument for the first time in a budget meeting.

James touched on this in the session's closing exchange. The organisations that managed to fund and sustain significant supply chain transformation were not the ones that found a better way to sell a business case. They were the ones that understood the underlying economics of the business well enough to explain supply chain's contribution to those economics, and then built the case from there, in language that connected to the decisions the board was actually trying to make.

That is a harder piece of work than reframing from cost-out to resilience. But it is probably the more durable one.

This discussion was part of BestPractice.Club's Spring 2026 programme. The in-person session on 29 April in London continues this thread. Details at bestpractice.club/upcoming-sessions.